Equifax and TransUnion are two of the largest and most reputable credit bureaus in North America. Both companies provide credit reports, one of the most vital tools you can use as a landlord to screen tenants.

But is one credit bureau better than the other? After analyzing a selection of Equifax and TransUnion credit reports, we’ll break down the main differences between them so you can make an informed choice.

Credit scores

It’s no surprise that there was a difference between the Equifax and TransUnion credit scores, as each credit bureau has their own proprietary formula to calculate these scores. What’s interesting to see is just how different the scores were. Generally, the TransUnion scores were higher than the Equifax scores.

Here’s an example of the same individual’s scores compared between Equifax and TransUnion, with a difference of 142 points.

In the example below, depending on where these scores fall in the range, this might be the difference from the applicant being selected or not.

TransUnion and Equifax scores can vary drastically: 42% of the time, there is more than a 40-point difference in the score between the two bureaus.

To understand the potential cause behind this major difference in reported credit scores, we compared hundreds of TransUnion and Equifax credits reports and highlighted the key points below.

Total debt

We were surprised to see a significant difference in total debt reported between Equifax and TransUnion. One possible reason could be that since there’s a cost to report to a credit bureau, most businesses would report to only one bureau and not the other.

This data point underlines the importance for small landlords in getting reports from both bureaus.

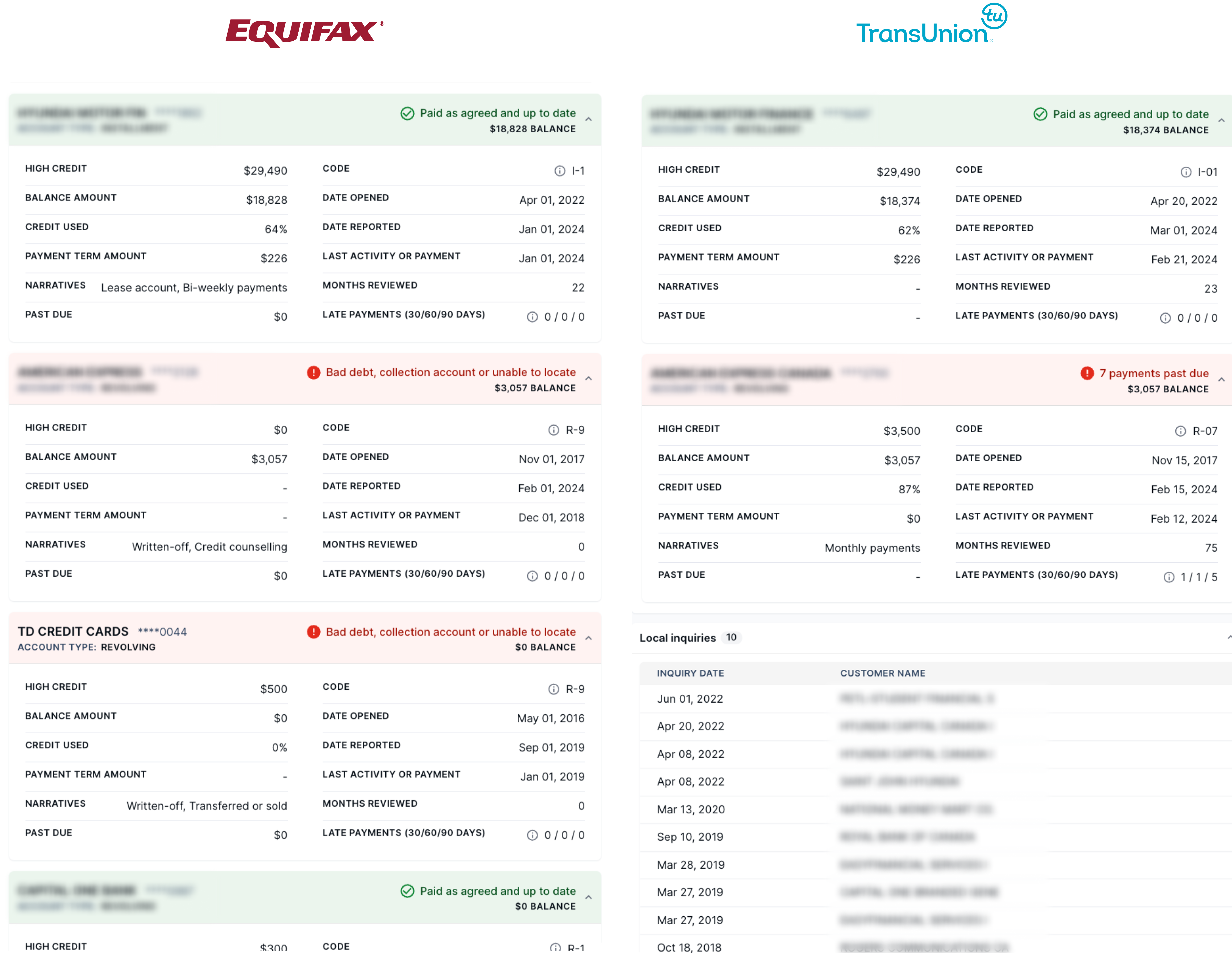

In the example below, Equifax found a mortgage on an individual’s credit report, while TransUnion did not list that mortgage.

Monthly debt payments

In our comparison, the monthly reported debt payments were nearly the same between the Equifax and TransUnion credit reports. This was driven by the data from each individual’s financial products, which appear as tradelines.

This is interesting because as we review those tradelines, the data is quite different. This tells us that the Equifax and TransUnion criteria for displaying tradelines varies.

Of the credit reports that we compared, only 2% had a hit that was not reported by the other credit bureau. If we include more credit reports in our comparison, we expect to see these cases increase, which highlights the importance of getting both Equifax and TransUnion reports to ensure no important data is missed.

Reported (billing) addresses

Reported addresses are those that are used for billing purposes when an individual has opened up a product or service. This could be for items such as a cell phone or a streaming service.

Reported addresses are valuable for landlords because they give them the ability to cross-reference an applicant’s rental history with the addresses found in the credit report. If a match is found, you can be more confident that the information provided by the rental applicant is accurate.

Nearly one-third of reported addresses were found on only one bureau’s credit report. Of those missing addresses, nearly an equal split of them were reported to a single bureau, meaning neither Equifax or TransUnion had an advantage.

As each bureau had its own unique reported addresses, it’s essential to have data from both credit reports, especially considering the importance of verifying rental history during the tenant screening process.

Tradelines

An overwhelming 96% of all the credit reports we reviewed had a hit on tradelines. This makes sense, as both credit bureaus report on existing products, like loans and credit cards. TransUnion credit reports generally displayed more tradelines with more historical data.

From a landlord’s perspective, seeing more tradelines gives a higher degree of confidence that the rental applicant is managing their finances well, especially if these tradelines have been paid out.

Here’s an example where Equifax showed an overdue tradeline while TransUnion did not report the same tradeline.

The bottom line when it comes to tradelines? Less than half the time, both bureaus showed the same lenders, so by running only one credit report, a landlord is at risk of missing key information like a loan that may have been late or gone to collections. The chances of that happening are high at 55% of the time.

Collections

A collection is an unpaid, overdue bill (over 90 days) that has been written off and sent to a collection company.

The majority of people don’t have collections, which matches our analysis: out of all the credit reports we reviewed, most reported no collections. When we look at the collections that were found, 59% of the time, both bureaus reported the same number of collections. However, the collections didn’t match 41% of the time. There was also an average of 1.3 differences in non-matching collections.

TransUnion had a small advantage because it returned slightly more collections. Still, to get a full picture of your applicant, running credit reports from both bureaus would ensure you capture all of this data, as there’s a 41% chance you may miss a collection.

Here’s an example of how collections are reported differently across both credit bureaus:

Reported employers and local inquiries

While Equifax and TransUnion report on a person’s employment history and any related local inquiries, this data rarely matched across both bureaus. For this reason, having two credit reports will give you a more complete profile of your rental applicant so that you can make a more informed decision.

Our final thoughts

The results between the two bureaus were noticeably different. Key aspects like reported tradelines and collections varied, which explains why credit scores were different between the bureaus. Each credit bureau also has its own formula to calculate credit scores, which contributes to these variations.

Therefore, it’s critical to run both credit reports so that you don’t miss crucial information about your prospective tenant or potential red flags. Minimize this risk and start screening with SingleKey’s Dual Credit Report.